Identity fraud is growing into an increasing issue for the automotive industry, especially dealerships. The numbers are big. In 2023 alone, it was reported that the industry faced a loss of $7.9 billion.

This increase in fraudulent activity is forcing many US dealers to consider halting out-of-state sales, a decision that could increase costs for consumers amid already high interest rates.

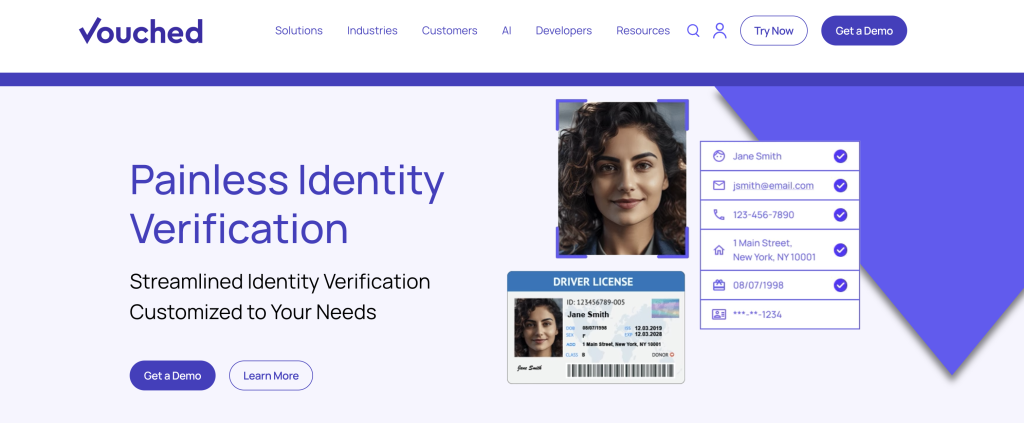

Digital identity verification company, Vouched, provides a ‘verification toolkit’ for those working in the automotive industry, enabling them to ensure every customer is legitimate by augmenting Vouched’s visual identity verification solution with digital data analysis, social security validation, and real-time driver’s licence validation.

We spoke to Peter Horadan, CEO, Vouched, to learn more about the issues fraud can cause the automotive industry and how the company can help.

Just Auto (JA): Who are Vouched and what does the company do?

Peter Horadan (PH): Vouched is the leader in online identity verification. When you’re having an online interaction with someone, and a username and password is not enough, but you need to know the real identity of the person that you’re dealing with, Vouched has great tools for this.

This comes up in lots of industries. A simple example is if you’re opening a bank account remotely online, the bank must verify your ID, they must verify that you are who you say you are. Vouched has a simple online process where a person can show their ID, show their face; we read them, we match them up, we do fraud detection behind the scenes, and we give that financial institution a strong idea that this person is, or is not, who they say they are.

What threats does fraud cause within the automotive industry?

We’re starting to see a new breed of identity fraud in the automotive industry, where several things have come together at the same time.

The first is identity theft or data dumps. How this works is you might receive a notice from a service provider saying that they’ve had a data breach, your identity was lost in that data breach and a fraudster has some of your personally identifying information.

We’re starting to see a new breed of identity fraud in the automotive industry, where several things have come together at the same time.

That data is now out there and it’s easy to get. For fraudsters, it’s relatively easy to go get those files and have at least some of the personal identifiable information of the person. That is then combined with the ability to make extremely good physical fakes, and to do that remotely.

There are several websites where you can pick the jurisdiction you’re interested in, such as a US state or a country, find that ID, then upload your information. You could upload whatever picture you want, you enter the name, address, the birthday that you’d like, and then you pay. In the US it costs about $130.

Two weeks later you’ll get a box of socks in the mail, and inside one of those socks is a perfect physical identity that matches what you’ve uploaded. A lot of the security features are intact; the UV light test passes, any 3D or holograms pass, the bar code on the back passes. You can then use that physical identity, which now contains some real information from some identity you’ve stolen, and some information that you’ve maybe manipulated to make things easier for you, and then go and in person to identify yourself as someone else.

This affects automotive, because people then go buy a car under a fake identity using credit. They drive off with the car, and then once it’s discovered, the dealership is on the hook because they will not be funded for that fraudulent loan.

How does this impact consumers?

They’re going to find that prices go up. The dealership costs must go somewhere, and often they’ll get passed on to consumers. Fraud impacts all of us with the increase in prices to make up for it.

Consumers are seeing more rigour and more standards around if you do purchase a car. You’re going to get looked over several times, as opposed to maybe an easier process in the past.

What consumers will see in the future is we’re going to have new forms of identity designed to combat this kind of fraud, and those will take the forms of something called a mobile driver’s licence or a digital identity. This world is still being invented, but I would hang a ‘coming soon’ sign out front; there will be new ways of identifying yourself that are far more resistant to fraud.

The way we identify ourselves today hasn’t changed much since the early 1900s.

The way we identify ourselves today hasn’t changed much since the early 1900s. This idea that you have a physical document that’s meant to stand on its own is quite an antiquated idea, and there’s a lot of technology that we could use to make this much better.

Why do you think the way we identify ourselves hasn’t developed as fast as other technology has?

Computers have been around for a long time and taken over our lives, especially when you think about how much we use our mobile phones. Yet we have a long way to go in automating workflow; there are so many manual processes still in this world that we are just getting started in terms of automating manual processes.

If you’ve ever received an invoice as a PDF in your email, it’s really quite an odd thing. It’s digital because it’s in your email, but you can’t pay it automatically. You can’t enter it into your accounting system. You still have to open it, read it, enter it into your accounting system and pay it.

What solutions can Vouched provide the industry?

There’s a new breed of tools that have become available that dealerships can use to help. We have an online tool. It’s a subscription service where we would ask for the identifying information the person has provided, maybe even that they show their face to the web camera, and then we will use facial recognition and identity verification.

Then behind the scenes, we’ll do proprietary fraud checks to say, does it make sense, does the picture match, do the other details match, does it make sense that a person with this identity would be here at this place in time? Then we’ll provide a fraud score or a risk score to the dealership. We can provide a lot more sense of certainty beyond just simply looking at an ID.

There are databases that have been compiled from public sources, social media and other places, of what people look like. We also use longitudinal data about a person, such where do we think they work, and is it reasonable that they would be here given where they work. We can ask, have we seen them in this area before? Alongside matching data such as is this a known address for this person? Is this a known phone number? Is this a known email?

One of the one of the big indicators is how long has this phone number been associated with this identity, or how long has this email been associated with this identity?

For example, someone comes in to buy a car. We use an online tool to say we know that this email is associated with this identity; we then send them an email and ask them to tell us the code that was in the email so that we can verify that they have received that email. That’s a new technique that people are using as a type of second factor (‘two-step’) in our identification. One big tell is if that email was created last week. That doesn’t mean for certain that we have an identity theft problem, but it’s certainly something to take a look at. Whereas, if that email is created twenty years ago, you can have a lot more feeling of comfort.

What do you see the future holding for this issue?

I think the first thing that we can expect to see, unfortunately, is on the negative side, where we’re seeing identity fraud become easier and easier. These AI tools that have been created mean you can create deep fakes quite easily. As soon as you have a visual likeness, a voice, other identifying data, you can then use that to create a fraudulent identity that’s quite convincing. AI can be a force for bad and a force for good.

I think a second thing we’re going to see is people are going to start to use AI to do things on their behalf. For example I have an AI travel agent and I say to it; “I’d like you to find me a rental car, I’d like a good price, have it ready at this time and at this place.” If you’re in the car business you won’t have a person showing up, you have an AI agent saying: “I’m working on behalf of this person.” How do you know whether to trust that?

You might think you could ignore that problem, but these AI agents are going to be quite useful, and so people are going to want to use them. It’s something over time we’re going to have to deal with.

On the one hand an AI might be fraudulently impersonating someone, but on another hand, an AI may be legitimately doing things for someone. How do we include that in our society? How do we identify that?

The interesting thing about mobile drivers’ licences is you can, with cryptographic surety, prove that it’s a valid licence issued by the government, which you can’t do with the physical ID. Physical IDs rely on UV lights and holograms which can all be copied. Whereas with the mobile driver’s licence, where it’s on your phone, there is a cryptographic proof to prove that it was issued by a government.

All these things are going to combine to change how we identify ourselves in the future.

Originally published on Just Auto. For more details, visit the source.